I remember the day I finally set up an automated expense tracker. I connected my primary bank account and my credit card to an app that promised to do all the work for me. It felt like I had finally cracked the code to financial freedom. No more manual entries. No more guessing where my money went.

For about a week, it was magical. I watched my dashboard update in real-time. I saw every Swiggy order and every UPI payment to a local kirana shop appear as a neat little bar on a chart.

But then, the anxiety started to creep in.

The privacy trade-off

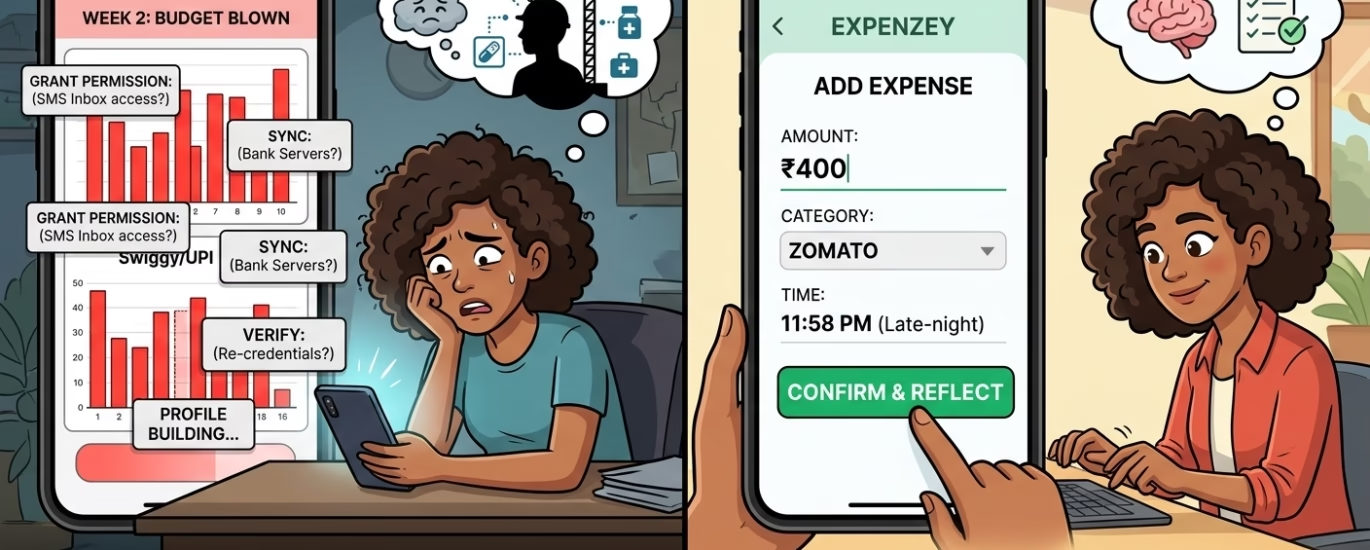

The app kept asking for more permissions. First, it was just “read” access to my SMS inbox to scan for transaction alerts. Then, it wanted permission to sync with my bank’s servers. Every time the app updated, I had to re-verify my credentials.

I started asking myself: what exactly are they doing with this data? These companies don’t make money just by being helpful. They make money by building a profile on my spending habits, my lifestyle, and my weaknesses. Do I really want a third-party app knowing exactly how much I spent at a bar on a Friday night or which specific pharmacy I visit?

The illusion of control

Automation is a double-edged sword. When the app does everything, you stop paying attention. Because I wasn’t the one typing in the numbers, I felt detached from my spending. I would get a notification saying I’d blown my budget, but it felt like a passive observation rather than an active choice.

It’s easy to ignore a red bar on a screen. It’s much harder to ignore the physical act of logging an expense you’re not proud of. That friction—the very thing these apps try to remove—is actually the most important part of managing money.

Why manual tracking is actually better

When you manually log an expense, you have to stop and think for three seconds. You see the amount. You see the category. You acknowledge the transaction.

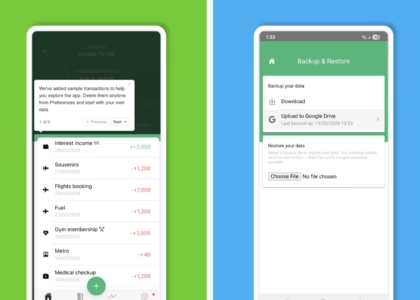

This is where Expenzey comes in. I stopped using the “set it and forget it” apps because they were making me mindless. With Expenzey, I log my expenses manually. It takes me less time than it takes to scroll through Instagram, but it forces me to confront my habits.

If I spend ₹400 on a late-night Zomato order, I have to open the app and type it in. I have to look at the number. It’s a small, honest moment between me and my bank balance.

The danger of “categorization”

Have you noticed how bank-linked apps often guess your categories wrong? You buy a pack of cigarettes at a grocery store, and it tags it as “groceries.” You transfer money to a friend via UPI, and it gets tagged as “miscellaneous.”

Because the data is automated, you stop correcting it. You end up with a messy, inaccurate view of your life. Manual tracking allows you to use labels that actually mean something to you. I don’t need a corporate category like “utility bills”—I need a label like “stuff I keep forgetting to pay” or “guilty pleasures.” Expenzey is built on the idea that you should define your own financial narrative, not some algorithm.

Breaking the cycle of guilt

Bank-linked apps are designed to be “helpful,” which often translates to constant alerts. “You’ve spent 80% of your budget!” “You’re spending 15% more than last month!”

These notifications don’t help you save; they just make you feel like you’re failing. Constant reminders of your “bad” behavior don’t create better habits. They just create stress. I prefer a quiet interface. Expenzey doesn’t judge my spending or send me guilt-tripping notifications. It’s just a tool, like a pen and paper, that sits there waiting for me to be ready to record my day.

Finding your own system

If you feel like you’re losing track of your money despite using an automated app, try switching to a manual system for just one week. Don’t worry about the perfect category or the “right” way to do it. Just record what you spend.

You’ll be surprised by how much more aware you become. You might find that you don’t need a complex algorithm to tell you where your salary disappears by the 15th—you’ll realize it the moment you type it into your phone.

Start simple

Financial awareness isn’t about fancy charts or deep data integration. It’s about building a relationship with your money. If an app is doing the thinking for you, you aren’t really in charge of your finances.

Take back control. Download an app that respects your privacy and asks you to participate in your own life. Start small, stay consistent, and remember that you don’t need to link your bank account to start living within your means.